The New Zealand government gets most of its revenue from taxes on:

- individual income

- business income

- goods and services

This article gives an overview of how income tax works for individuals and businesses.

You can also learn more about GST in our article GST Explained here.

Income tax on individual income

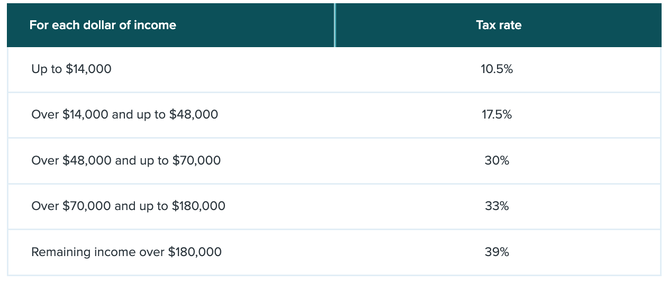

How much income tax you pay depends on how much income you earn. Our tax system is a progressive system, which is different than just paying the same flat tax rate on every dollar you earn.

From 1 April 2021 New Zealand’s individual income tax rates are:

Your individual income could include:

- salary or wages

- Work and Income benefits

- schedular payments (made to contractors who perform certain activities)

- interest from a bank account or investment

- earnings from self-employment

- shareholder salaries

- money from renting out property

- overseas income

Some income is taxed before you get paid. This includes salaries, wages, Work and Income benefits, schedular payments and interest. The amount of income tax your employer or payer deducts depends on the tax code and income information you gave them.

You might get an income tax refund or have income tax to pay at the end of the tax year if you've been taxed at the wrong tax rate during the year. It's important to use the correct tax code.

Tax codes are lettered codes that you need to put on the Tax Code Declaration Form (IR 330) from the Inland Revenue Department (IRD), which your employer should give to you when you start a new job.

The most common tax code is M.

This means the job that the IR 330 form is for is your main/highest source of income, and:

- You do not need to pay off a New Zealand student loan,

- You do not have an annual income between NZ$24,000-$48,000,

- and are not entitled to Working for Families Tax Credits or NZ Super, Veterans Pension or any overseas equivalent.

If the IR 330 form is for a job that isn’t your highest source of income, then you need to supply a secondary income tax code.

Your secondary income tax code is determined by how much your combined annual income is and whether you are paying off a student loan.

For example, if your annual income from all sources is between NZ$14,001 and NZ$48,000 your secondary tax code is S.

You can work out your tax code or check it’s correct on the IRD website here using their tax code questionnaire.

Some income is not taxed before you receive it. This includes income from self-employment or renting out property, and some overseas income.

You pay income tax on this income at the end of the tax year. The amount of income tax you pay depends on your total income for the tax year.

A common misconception is that you pay all of your income tax at the same tax rate. You just find what band your income is in, and then you pay that tax rate on all of your income. Under this system, someone earning $50,000 would pay 30% tax on every dollar they earned. But that’s not how income tax works in New Zealand.

If someone earns more than $14,000, they’ll pay 17.5% income tax, but only on their income above the $14,000 threshold. If they earn more than $48,000, they’ll begin paying 30% income tax, but again, this higher tax rate will only apply to their income above $48,000. It continues in this progressive way.

For example: If you earn $30,000, you pay 10.5% on each dollar earned up to $14,000, and 17.5% on the next $16,000. So in total, you pay $4,270 - not $5,250, which is what you’d pay if you had to pay the same 17.5% tax rate across all your income.

You can work out the income tax on your income using the tax calculator on the IRD website here.

Who needs to complete an individual income tax return?

You need to complete an income tax return at the end of the tax year if you received more than $200 (before tax) in income without tax already deducted. This commonly includes income from:

- self-employment

- overseas

- rental property including Airbnb & Bookabach etc

- wage subsidies

- shareholder salaries

- 'under the table' cash jobs

- an estate, trust or partnership

You will need to complete your income tax return by 7 July unless you have a tax agent or an extension of time.

Need help?

If you think you need to complete an individual income tax return and would like some help then please don’t hesitate to contact us.

Income tax on business income

Businesses pay income tax on their profit (their income, minus any expenses).

Companies and corporates are taxed at a flat tax rate of 28%, unlike individual tax rates which are progressive.

Generally, businesses file their income tax returns at the end of their first year of business and pay their income tax in a lump sum at the end of the year.

After the first year, they pay in instalments called provisional tax.

What is provisional tax?

When you become subject to provisional tax you are required to pay income tax instalments during the year rather than a lump sum at year end. These instalments are most commonly based on the prior year’s income but there are several methods that can be used, which are discussed further below.

The amount of provisional tax you pay is then deducted from your tax bill at the end of the year.

Both companies and individuals can be subject to provisional tax.

Provisional taxpayers often earn income from:

- self-employed income

- rental income

- income earned as a contractor

- income from a partnership

- overseas income.

Provisional tax is payable where there is more than $5,000 of residual income tax payable at the end of the year.

What is residual income tax?

Tax to pay at the end of the year is called residual income tax.

Residual income tax is the amount of income tax you pay for the year, less any tax paid and other tax credits you may be entitled to.

Residual income tax is shown as a separate line in the tax calculation of your income tax return.

When you file your income tax return and calculate your residual income tax for the year, you deduct the provisional tax you paid earlier.

If you have paid more provisional tax than you actually owe, you will receive a tax refund from the IRD.

However, if you have not paid enough provisional tax to cover the residual income tax for the year, you will have to pay terminal tax.

For most, terminal tax will be due on either 7 February (or 7 April if you have an accountant with an extension of time arrangement) the following year.

How is provisional tax calculated?

The amount of provisional tax you pay is based on your expected profit for the year. There are four ways to calculate it.

Standard — the default option. Your last year's tax to pay + 5% (or your tax to pay from two years ago plus 10%).

Estimation — you estimate what you think your tax bill will be for the year. This can be a good option if you expect your income to be lower than last year.

Ratio — worked out as a percentage ratio of your GST return. This can be a good option if your income fluctuates a lot.

AIM — the accounting income method — is a new option that works through accounting software. It allows you to pay smaller amounts, more often, based on your current year’s cashflow. Your accounting software does all the calculations for you, at the same time as it works out your GST.

The due date and amount of installments you need to make for payment of your provisional tax each year depends on your balance date, which of the above options you use, and how often you pay GST (if registered).

If you have a 31 March balance date and use the standard or estimation option, provisional tax payments are due on:

- First installment 28 August

- Second installment 15 January

- Third installment 7 May

What happens if I don’t pay my provisional tax on time?

In short, bad things.

As well as incurring IRD interest from the date payment was due, late payment penalties may be charged.

Try and avoid these common pitfalls to stay on track with your income tax:

- Failing to set money aside for your tax bill, you don't want to end up with a big bill and no way to pay it.

- Not filing or paying your tax on time, you'll be charged a penalty if you file late, and interest on any overdue payments.

- Not keeping records of your income or expenses, or not keeping them long enough. You are required to keep all records for seven years by law.

Need help?

If you would like some help understanding or managing your business income tax obligations then please don’t hesitate to contact us.